Click here for our index which tracks the private sector.

The average funded ratio of pension plans remained stable in Q2 2024, while the solvency ratio improved slightly.

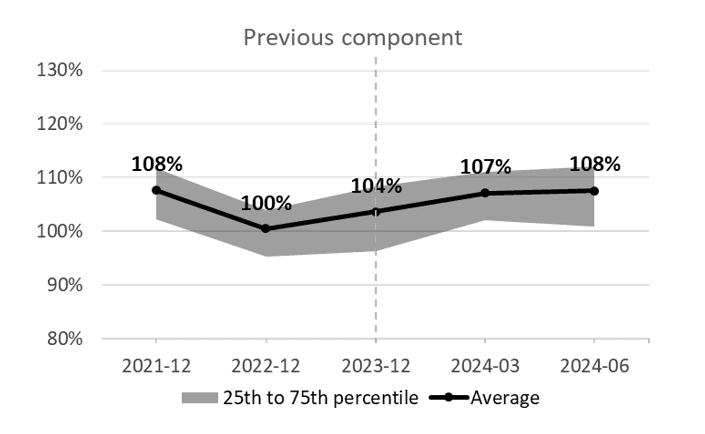

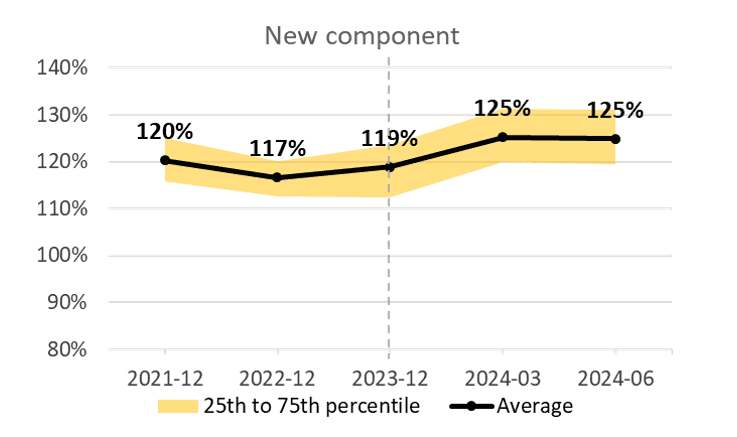

As at June 30, 2024, the average funded ratio of municipal and university sector pension plans is 108% for the Previous component and 125% for the New component (the components are distinguished by years of service accumulated before and after January 1, 2014, for the municipal sector and January 1, 2016, for the university sector). The ratio for the Previous component is up 1% in the second quarter and up 4% since the beginning of the year. The ratio for the New component remained stable in the second quarter, but is up 6% since the beginning of the year.

Note: The illustrated going concern financial positions are adjusted to include the full market value of assets, and therefore include the reserve in the Previous component and the stabilization fund in the New component, and exclude the effect of asset smoothing.

The financial position changed little in Q2 2024. Investment performance was similar to expected returns, and although the discount rates used to value pension plan liabilities increased, this increase was not significant enough to have an impact on the financial position. Current service costs changed little in Q2 2024.

The average solvency ratio for municipal and university sector pension plans as at June 30, 2024, is 103% for the Previous component and 114% for the New component. The ratio for the Previous component is up 1% in the second quarter and up 3% since the beginning of the year. The ratio for the New component is up 2% in the second quarter and up 3% since the beginning of the year.

The slight improvement in the solvency financial position in Q2 2024 is mainly due to a decline in actuarial pension plan liabilities. The discount rates have increased more on a solvency basis than on a going concern basis.

On June 5, Canada became the first G7 country to cut its key interest rate, lowering it by 0.25% to 4.75%. This is the first cut since March 2020, and other central banks have followed suit, including the European Central Bank. On the bond markets, despite a general decline in interest rates following this announcement, long-term rates still rose slightly during the quarter. The Bank of Canada is cautious about the persistent risks of inflation above their 1-3% target. Bond markets are now anticipating fewer key rate cuts for the year than initially expected. The impact on the Canadian dollar will also need to be monitored, as this rate cut widens the gap with the U.S. Federal Reserve’s 5.5% rate, which remained unchanged in June.

Meanwhile, the frenzy in the main stock market indices in the first quarter has faded, with more modest returns in the second quarter. The technology, telecom and utilities sectors continued to deliver positive returns, generally speaking, but returns from other sectors were mostly negative.

After a difficult 2023 for real estate investments, when the higher interest rate environment reduced real estate valuations overall, some private real estate funds are showing stabilized returns since the start of 2024. As for infrastructure investments, most continued to generate returns in line with expectations.

In April, the Canadian Institute of Actuaries (CIA) published a new mortality improvement scale. The CIA’s study highlighted significant trends in longevity and suggests that life expectancy will increase at a faster rate than previously predicted. For pension plans, this would mean higher-than-expected costs. Although the CIA and the pension industry have not yet decided on the use of this new scale, pension plan administrators could anticipate the potential impacts in a number of ways:

- Add an additional margin to the discount rate to reflect the approximate increase in liabilities and current service cost associated with the new mortality improvement scale.

- Transfer longevity risk by purchasing an insured annuity contract.

- Obtain advice from the plan’s consultant on risk management best practices, taking into account the specific context of the plan.

The CIA is also working on updating Canadian mortality tables and expects to publish the results of this analysis by the end of the year.

Our expert mortality teams can analyze the longevity risk specific to your plan and propose appropriate measures for its funding. Want to learn more about developments surrounding the mortality assumption? Contact your Normandin Beaudry consultant or email us.

The Normandin Beaudry Pension Plan Financial Position Index is calculated by projecting the pension plan financial data of its clients in the Quebec municipal and university sector. A separate index is published for the plans of Canadian clients outside of this sector. Assets are projected based on the performance of market indices. Liabilities projected on a going concern basis use an estimated discount rate based on each plan’s asset allocation and the sensitivity of asset classes to changes in interest rates on Government of Canada bonds. The discount rates used on a solvency basis are those prescribed by the Canadian Institute of Actuaries, and those for transfer values are therefore based on the previous month’s market interest rates.