The way obesity is perceived has changed significantly over the years, and the medical community now recognizes obesity as a chronic disease. This step forward has highlighted the important role of proper care in improving the overall health of those affected. Proactively managing this disease can prevent numerous complications and comorbidities, such as type 2 diabetes, cardiovascular disease and certain types of cancer¹. In contrast, the lack of appropriate treatment can negatively impact the person’s quality of life and increase long-term health care costs.

COVERAGE UNDER PROVINCIAL PLANS

Although the medical community now considers obesity to be a chronic disease, public health insurance plans in Canada do not cover obesity medications. However, a trend is emerging: on March 4, Alberta became the first province to officially recognize obesity as a chronic disease, helping to reduce the stigma around it².

COVERAGE UNDER PRIVATE PLANS

Historically, group insurance plans in Canada have explicitly excluded obesity drugs. However, private insurers have gradually expanded their coverage to include these treatments, which meet a growing demand from employers and beneficiaries looking for comprehensive health care options that are tailored to today’s needs. Some major insurers have integrated these drugs into their standard coverage, unless the policyholder chooses to exclude them.

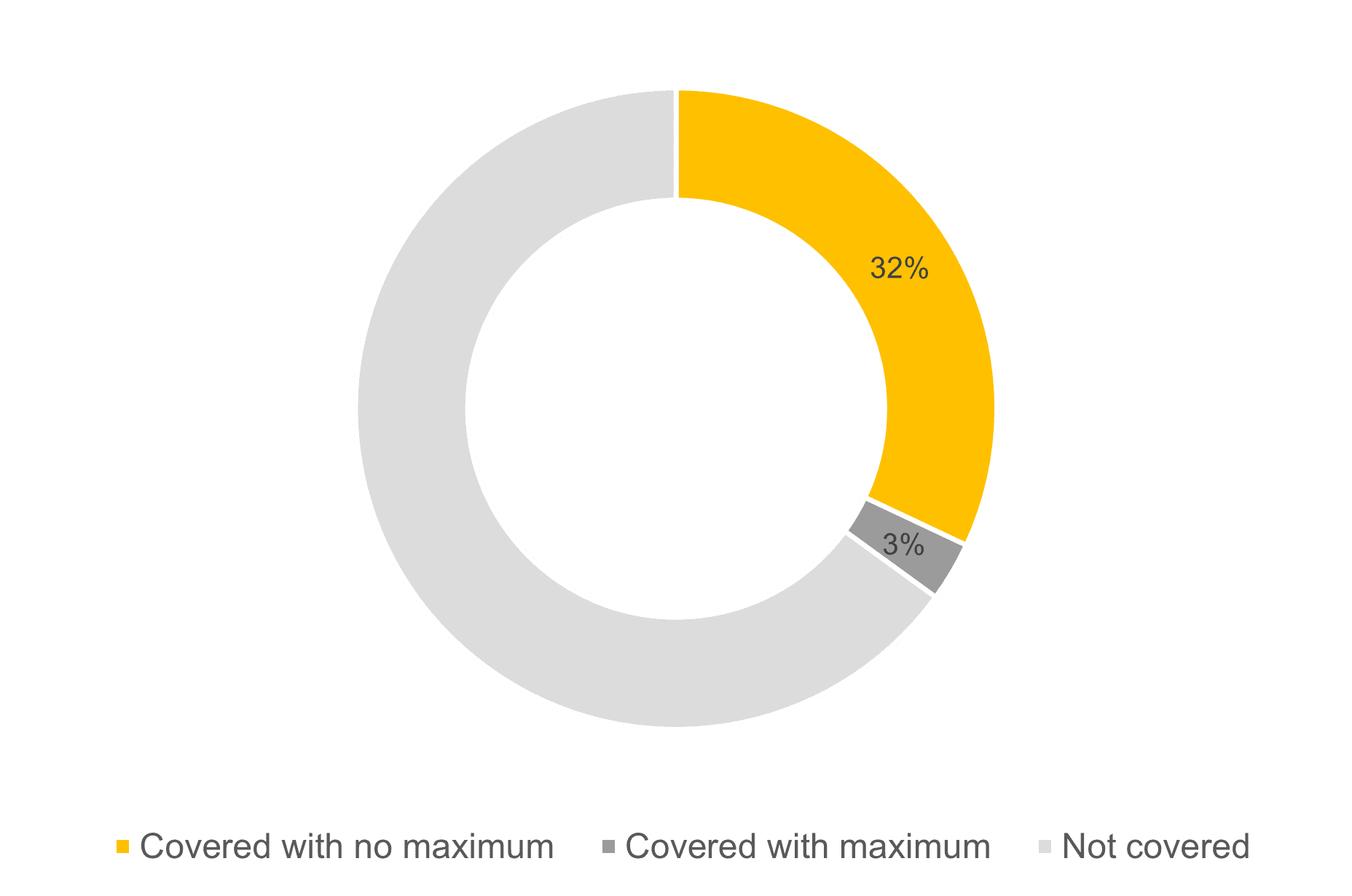

Overall, the number of group insurance plans covering obesity drugs is increasing. According to the 2025 edition of our total rewards survey, remun, 35% of organizations now cover these drugs. The following chart shows the provisions observed on the market.

EVOLVING PLAN COSTS

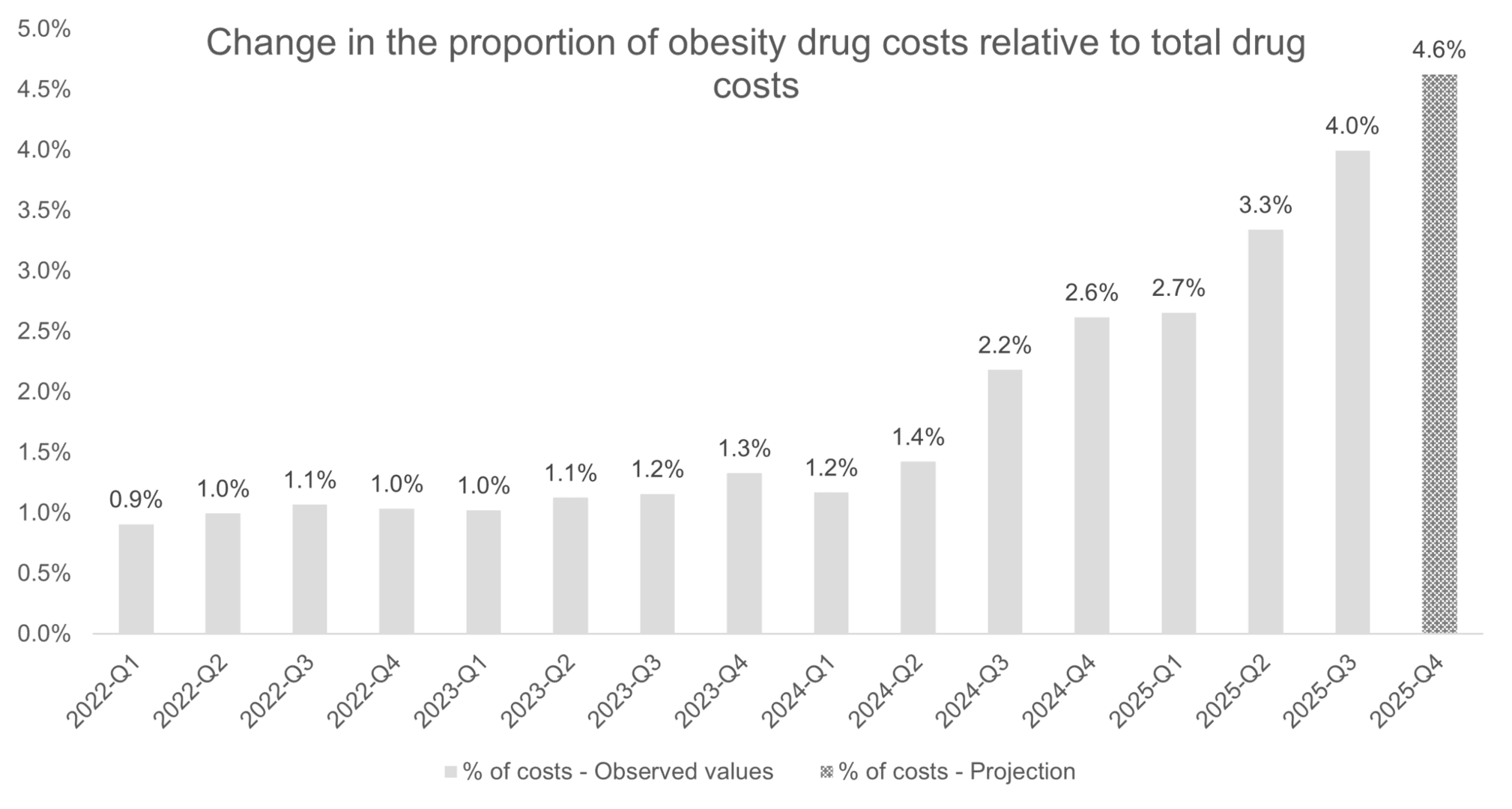

Until recently, obesity drugs represented a relatively low proportion of costs in private plans, due to the limited use of marketed drugs. However, since 2024, the arrival of new drugs has led to a significant increase in utilization. The following chart illustrates the change in the proportion of claim costs for obesity drugs relative to total drug costs. It also includes a projection for the last quarter of 2025 based on market data collected by Normandin Beaudry.

The increased coverage for these treatments is expected to have an impact on group insurance premiums. As a general rule, an increase in health insurance premiums of 3% to 4% would be required to account for the increase in claims. Organizations therefore need to look at ways to strike a balance between the coverage offered and cost management, while setting aside a sufficient budget to cover the addition of these drugs. If needed, changes could be made to their offering to fund this group insurance plan enhancement. However, it is not always possible or advisable to reduce other coverage. In such a case, it becomes important to rigorously manage claims to optimize the experience of beneficiaries while maximizing the investment made.

In the current context, insurers are becoming strategic players. To ensure that treatments are reimbursed based on recognized and objective medical criteria, various mechanisms have been put in place, particularly the prior authorization process. Although all insurers have these types of mechanisms, some have adopted more innovative practices than others.

FOOD FOR THOUGHT

Obesity drug coverage under private group insurance plans plays a crucial role in providing many Canadians with access to treatment. It can also serve as a lever for talent attraction and retention, and fits into a broader perspective of inclusion and sustainable health management in the workplace. Nonetheless, it is important to remain vigilant, keeping the related costs in mind.

A prescription for obesity drugs is usually preceded or accompanied by efforts to change lifestyle habits. As a result, obesity management in the workplace should go beyond drug coverage and leverage programs that promote overall health by focusing on nutrition, physical activity, psychological support and raising awareness around stigma. Facilitating access to professional services in mental health, nutrition and/or physical activity, while adapting internal practices and policies, can greatly influence employee health and thereby have a positive impact on productivity. These measures also help to prevent other lifestyle-related health problems, such as diabetes and high blood pressure. In fact, several insurers and providers of employee and family assistance programs (EFAPs) now offer tools that are tailored to these issues. A first step can be to identify the resources that are already included in your total rewards package and actively promote them to employees.

———–

¹ https://obesitycanada.ca/understanding-obesity/health-impacts/

² Despite recognizing obesity as a chronic disease, Alberta does not cover obesity drugs.

For more information or to discuss strategies for effectively structuring your group insurance plan or health offering, contact our team of health and group benefits specialists or email us.