June 2023

Accounting standards applicable to future group benefits:

Assumptions used by Canadian organizations and latest updates

See the Latest Updates section for more information on the accounting standards for the public sector and those for pension plan financial statements.

Many private-sector organizations must include in their financial statements the recognition of their obligations toward defined benefit pension plans (DB pension plans) and other post-employment benefit plans, such as medical care plans offered to retirees (other benefits).

Again this year, Normandin Beaudry’s specialists analyzed the annual reports of Canadian organizations listed on the S&P/TSX 60 Index (the 60 largest organizations) and on the S&P/TSX Mid Index (mid-cap organizations) for which the fiscal year ended between September 30, 2022, and February 28, 2023.

This analysis included about 65 organizations from the S&P/TSX 60 Index and the S&P/TSX Mid Index that sponsor at least one DB pension plan. Of these organizations:

- More than 80% also disclose information regarding other benefits.

- 85% disclose their results in accordance with international accounting standards, while the others disclose them in accordance with U.S. accounting standards.

The following charts show the key economic assumptions used by the organizations analyzed for their DB pension plans and other benefits. The assumptions are those that were in effect at the end of the fiscal year considered and used to calculate the obligation at the end of the fiscal year.

Each chart shows how the assumptions have evolved over time. Medians are represented by a solid line and shaded floating bars represent the range from the fifth to the ninety-fifth percentile.

It should be noted that a number of organizations offer plans in different countries. Some organizations disclose assumptions for plans in Canada separately, whereas others disclose average assumptions for all countries. While this could have an impact on the range of results, the median remains representative of Canadian assumptions.

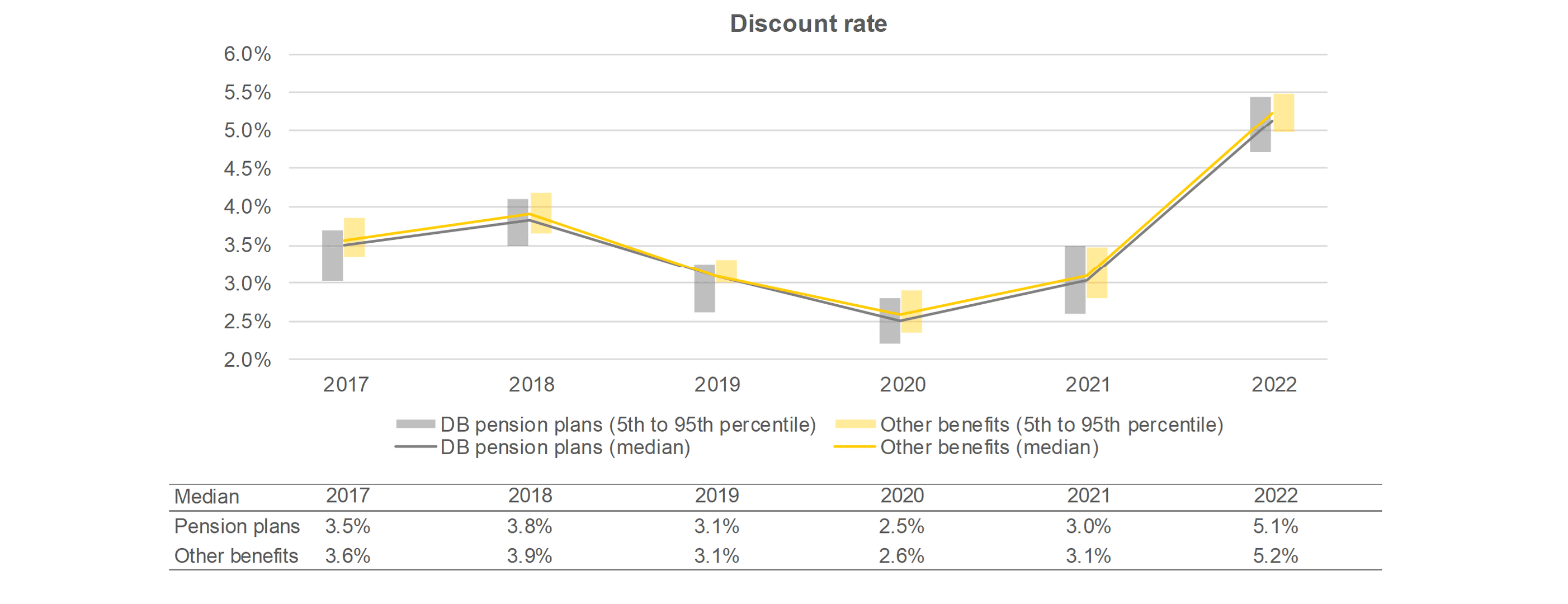

The discount rate is one of the most important assumptions. Because it is based on market rates, it can vary from month to month. The discount rate can also vary depending on the methodology used to determine the market rate, the plan’s maturity profile and the duration of the coverage offered (for example, a lump sum amount upon retirement or annual payments until age 65 rather than lifetime benefits). The obligation’s sensitivity to the discount rate variation depends on its duration. For example, for the same 0.1% decrease in the discount rate:

- a plan whose obligation has a duration of 10 years will see its obligation increase by 1%

- a plan whose obligation has a duration of 20 years will see its obligation increase by 2%

The following chart illustrates how the discount rates for DB pension plans and other benefits have evolved over time:

- The upward trend that began in 2021 continued sharply in 2022, reaching by far the highest discount rates of the past few years. This steep rise is mainly due to interest rate hikes by central banks.

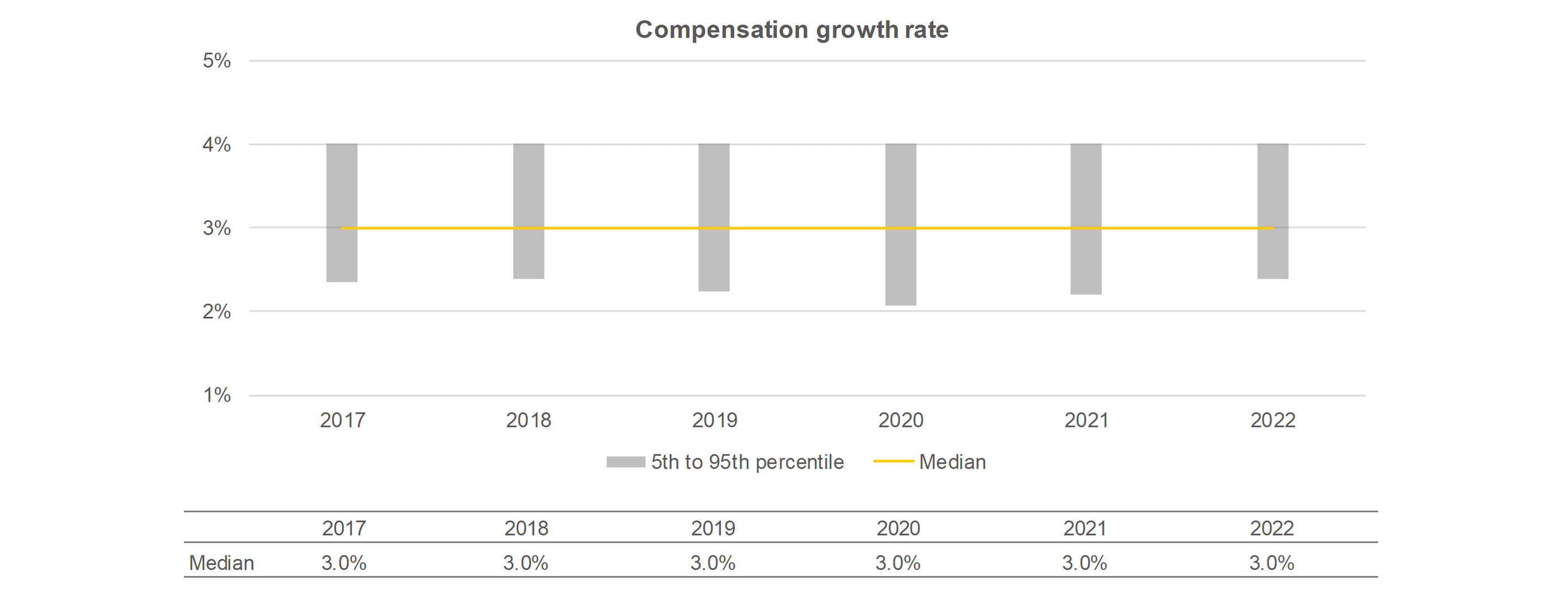

Many of the analyzed organizations sponsor DB pension plans and other benefits with entitlements based on salary at retirement. These organizations must therefore establish an assumption tied to the rate of increase in active members’ compensation.

The following chart illustrates how compensation growth rates have evolved over time:

- Despite the recent period of high inflation, the median of assumptions for the compensation growth rate remained unchanged in 2022.

- However, we noted that a few organizations had disclosed a higher assumption for the next two or three years compared to their long-term assumption. It will be interesting to see how this trend will evolve in the coming year.

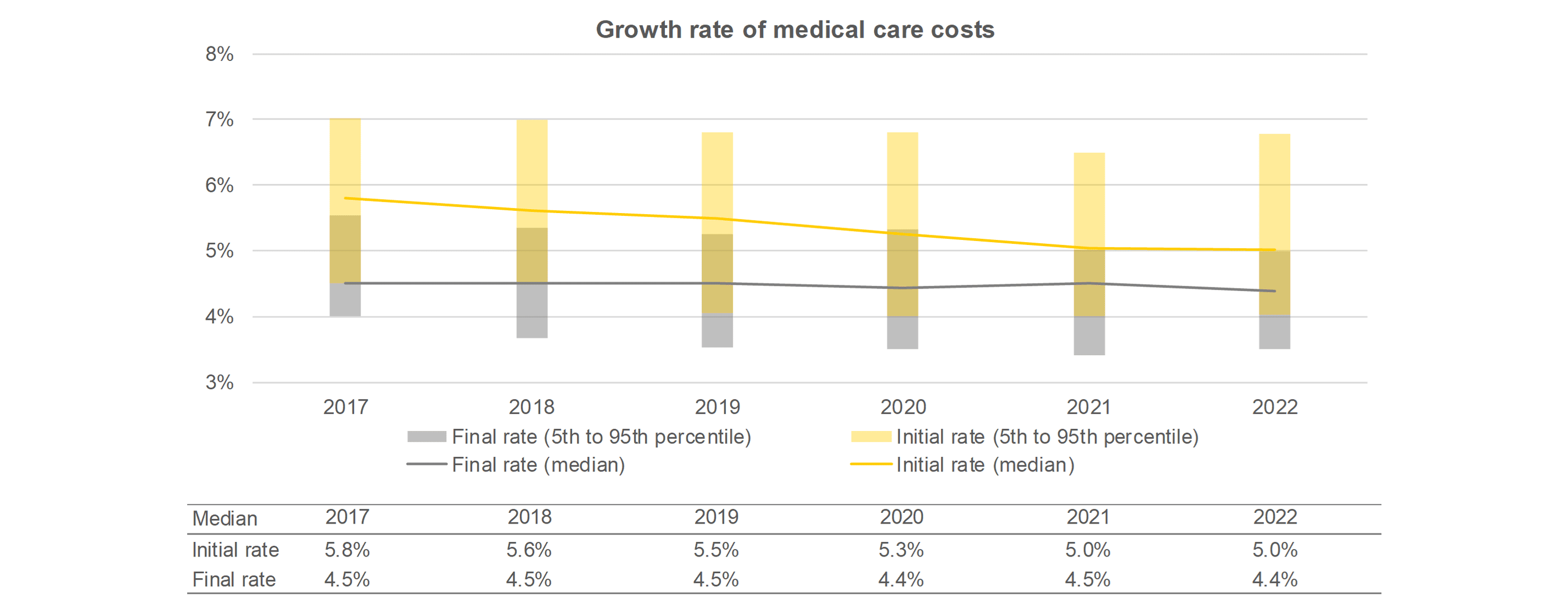

The growth rate of medical care costs is a very important assumption for group benefit plans offered to retirees, as it shapes future costs and its growth is higher than overall inflation.

Most organizations use an initial rate that decreases over a specified period into a final rate, to be applied to subsequent years. The initial rate can vary significantly from one organization to another compared to the final rate, which usually varies less.

The following chart illustrates how the initial and final growth rates of medical care costs have evolved over time:

- In recent years, there has been a general downward trend in the growth rates of medical care costs. However, 2022 was the first year in which the median of the initial rate assumption remained unchanged and in which a slight increase in this assumption was even observed in some cases. Once again, it will be interesting to see how this assumption will evolve over the coming year.

- The timeframe to reach the final rate can also vary significantly from one organization to another. About 70% of organizations that offer at least one health care plan to their retirees use decreasing rates, over a period ranging from 10 to 20 years for most organizations.

In its latest annual report, the Public Sector Accounting Board (PSAB) mentioned its decision to change the timeline for the employment benefits project in light of the many comments made on the project’s first exposure draft. The PSAB stated that an additional analysis and review of the proposed standard would serve the Canadian public interest.

This first exposure draft was published in late July 2021 and concerned the proposed Section PS 3251, pertaining mainly to deferral provisions (deferred recognition of actuarial gains and losses) and discount rates. The proposed standard would replace Sections PS 3250, Retirement benefits, and PS 3255, Post-employment benefits, compensated absences and termination benefits. See our August 2021 bulletin for a summary of the key proposed changes.

On December 16, 2022, the Accounting Standards Board (AcSB) published the amendments to Section 4600, Pension Plans, which outlines the requirements for the preparation of pension plan financial statements. By amending Section 4600, the AcSB wanted to tackle less complex problems that could be resolved quickly in order to improve the section’s relevance in the short term.

The main amendments relate to the following:

• Accounting treatment of insured annuity purchases

The amendments provide guidance on the recognition of insured annuity purchases and on related information to be disclosed. In particular, the following clarifications were made:

- Buy-in contracts must be measured at the amount of the corresponding obligation and are not considered investments to be measured at fair value. According to a clarification made in a new exposure draft published in May, information on investments measured at fair value is no longer required for this type of investment.

- For a buy-out annuity purchase, the asset and the corresponding obligation must be derecognized when the transfer of risks to the insurer occurs, under certain specified conditions.

- The information to be disclosed for these transactions differs according to the type of annuity purchase.

• Accounting treatment of plan splits or amalgamations

The revised section specifies the date on which a pension plan split or amalgamation is recognized. The date on which assets and obligations are recognized or derecognized, as the case may be, must be the latest of the following:

- the effective date of the transaction according to the adopted resolution;

- the date of regulatory approval of the transaction; and

- the date of transfer of the assets and obligations in connection with the transaction

In many cases, the transaction will be therefore recognized on the date of transfer of the assets and obligations. It should be noted that this new approach differs from that which is required for recognizing splits and amalgamations in the financial information presented in the Quebec Annual Information Return.

Information will be required in the financial statements to document the nature of the transaction and the status of its progress before it is recognized in the financial results.

• Presentation requirements for defined contribution plans and combination plans

The revised section states that a statement of changes in pension obligations for defined contribution pension plans does not have to be prepared. However, pension obligations must still be presented in the statement of financial position.

For a combination plan, that is, a plan with a defined benefit component and a defined contribution component, both components must be presented separately in the statement of financial position, in the statement of changes in net assets available for benefits and in the notes to the financial statements.

• Information on investments held in master trusts

Additional disclosure requirements on risks associated with investments held in a master trust will now have to be included in financial statements. The new information to be provided includes the types of investment assets and liabilities and fair value hierarchy of the types of investment assets and liabilities held by a master trust.

The changes will apply to fiscal years beginning on or after January 1, 2024. Earlier application is permitted. The AcSB is continuing its annual process of improving accounting standards for pension plans.

Our experts assist many clients in preparing their financial statements. We can help ensure that you are in compliance with the accounting standards. Contact us!