Manager underperformance in recent years casts doubt on active management in a market dominated by a few large US technology companies. In this context, is active management still a good way to gain exposure to stock markets? We will try to answer this question by analyzing the evolution of stock market characteristics and manager performance.

Markets have delivered above-average returns over the last 10 years, which has allowed many investors to improve their financial situation. However, over the same period, median manager performance has been below the benchmark, after management fees.

PERFORMANCE OF ACTIVE MANAGEMENT

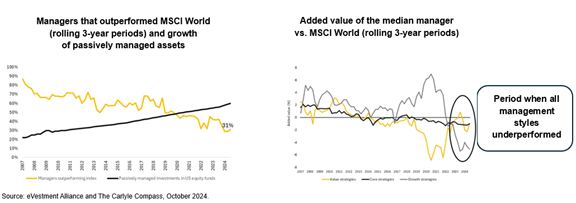

The proportion of global equity strategies generating added value has been steadily declining since the 2008 financial crisis. Since 2020, median managers have lost value, regardless of management style (value, core or growth).

How can the underperformance of managers with different management styles be explained?

ANALYSIS OF CURRENT MARKET PERFORMANCE AND RISKS

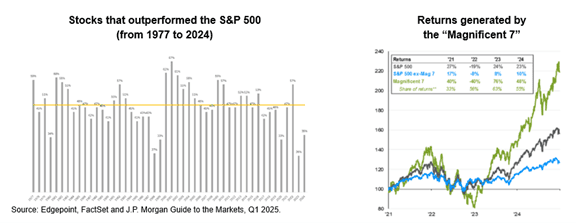

Since 2020, performance is attributable to a limited number of stocks. The number of stocks outperforming the S&P 500 is below the historical average, creating less opportunities for managers to stand out through stock selection. Magnificent Seven stocks[1], which represent 24% of the MSCI World and 33% of the S&P 500, have contributed over 50% of returns of the S&P 500 and 33% of the MSCI World since 2021.

Few managers have allocated more than 30% of their portfolio to these seven stocks, representing a high concentration risk in a single sector. For example, a portfolio with no Nvidia shares in 2024 would have resulted in a shortfall of around 3% relative to the global market.

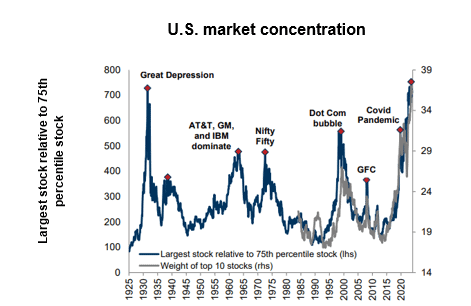

Market concentration and returns are at an unprecedented level. The weighting of the 10 largest stocks in the S&P 500 is the highest since 1925, reaching almost 40% and 26% of the MSCI World (in late 2024, the top 10 large-cap stocks in the MSCI World index were US companies).

Historically, index concentration has been cyclical. We could therefore see a drop in the concentration of indices over the next few years. History suggests an increased likelihood of a mean reversion, rather than sustained concentration.

A return to a more diversified performance environment, with a wider range of performing securities from a variety of countries and sectors, could be more conducive to active management. Indeed, over 75% of active managers outperformed the market over a three-year period after declining concentration, as experienced in the 1970s and after the bursting of the tech bubble in the early 2000s[2]

CAN WE RELY ON THE PAST?

Although global indices appear to present an increased risk due to their heavy weighting in a few stocks, there are two notable differences from other periods of high concentration:

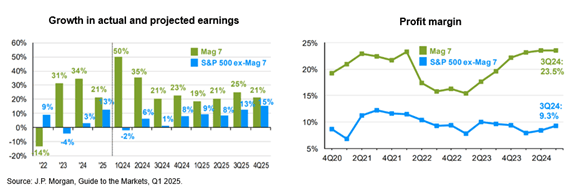

1. Large-cap companies are also those with the highest earnings growth and profit margins.

The performance of these stocks over the next few years will have a major impact on index returns. Currently, the risk seems to be more closely related to high expectations for earnings growth, whereas risk is normally linked to the financial quality of these companies.

2. The significant increase in passively managed assets is generating a positive feedback loop on the largest stocks.

The growth in the share of assets under passive management (see previous chart) benefits the largest companies. It gives them a cost-of-capital advantage and fuels their development, making them even more attractive. This trend is putting pressure on active managers as they build portfolios, particularly due to higher management fees, which result in managers being unable to outperform the indices. Meanwhile, the tendency has been strengthened by the rise of exchange-traded funds and easier access to online savings platforms, which generally favour passive investing to reduce costs.

HOW SHOULD YOU POSITION YOUR STOCK MARKET PORTFOLIO?

To summarize, despite index underperformance, high concentration can translate to greater risk for investors, even though the largest companies are showing sustained growth in earnings and higher profit margins. The structural trend toward passive management could even accentuate the level of concentration.

In such a context, the right approach is based on rigorous risk management and alignment with each investor’s investment objectives.

In our view, it’s not a question of active or passive management but rather of whether the stock portfolio is aligned with the long-term investment objectives. Here are a few questions that can help guide your decisions when building a stock portfolio:

- What is the objective of your stock market exposure and how significant is it in terms of your overall assets?

- What is your risk tolerance (is it a priority to protect capital and limit losses during market downturns)?

- Do you consider it crucial to integrate sustainable investing criteria, to select stocks that trade at reasonable prices close to their fundamental value and to avoid any sharp downturns?

The answers to these questions should guide your strategy. Once your strategy is established, its implementation is of critical importance. Given the significant difference in results between active and passive management in recent years, a meticulous and gradual implementation plan is to be prioritized.

If you’d like to take a closer look at the structure of your stock portfolio and ensure it aligns with your objectives, our team of investment consulting specialists is here to help.

This article was written by:

Raphaël Gariépy,

Principal, Investment Consulting, Normandin Beaudry

- [1] The Magnificent Seven are Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla.

- [2] Wellington Asset Management: An index isn’t a fiduciary — and six other concerns about the push for passive.