Normandin Beaudry Pension Plan Financial Position Index, June 30, 2026

Normandin Beaudry has updated its pension plan financial position index as at June 30, 2026, tracking defined benefit pension plans in Canada.

Normandin Beaudry has updated its pension plan financial position index as at June 30, 2026, tracking defined benefit pension plans in Canada. The information below highlights the segment specific to the Quebec municipal and university sector. Click the following link for our Canadian index, which excludes this sector.

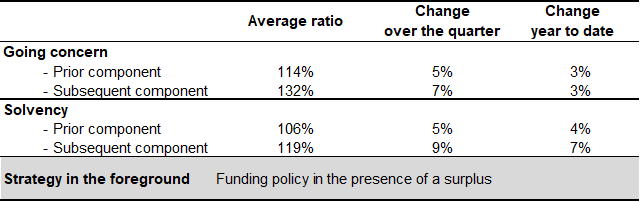

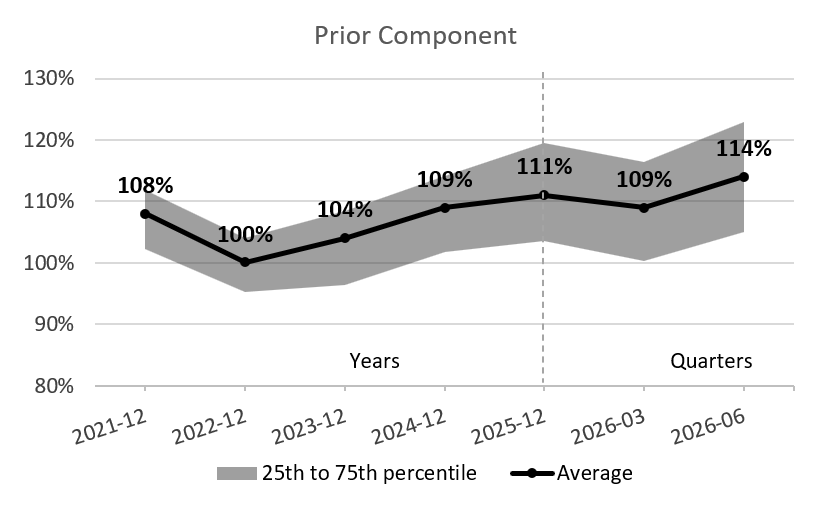

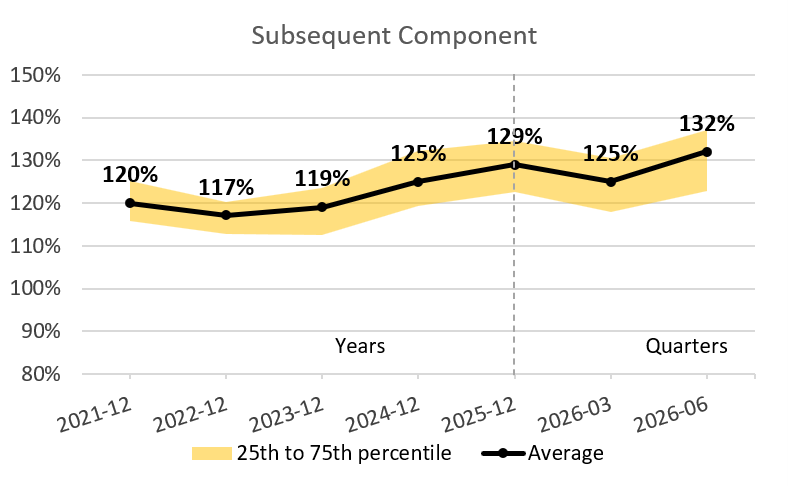

Note: The components are distinguished by years of service accumulated before and after January 1, 2014, for the municipal sector and January 1, 2016, for the university sector.

Our index tracks both funding valuation bases:

For the average pension plan, surplus increased during the second quarter of 2026, supported by favourable equity market returns. Although interest rates fluctuated during the quarter, they ended at a level similar to that observed at the beginning of the period, so their impact on the valuation of liabilities was limited.

The Canadian Institute of Actuaries (CIA) has announced its intention for the newly published mortality tables and improvement scale to be integrated into transfer values as of February 2027. Accordingly, the deterioration in financial position resulting from a more rapid increase in longevity would not be reflected before that date under the solvency basis. However, the effect of these new mortality assumptions may be recognized earlier in going concern and accounting results.

Note: The illustrated going concern financial positions are adjusted to include the full market value of assets. They therefore include the reserve in the prior component and the stabilization fund in the subsequent component, and exclude the effect of asset smoothing.

The second quarter of 2026 was marked by a rebound in equity markets, particularly in the United States, after the broad decline in March 2026 that followed the outbreak of war in the Middle East. Concentration in the U.S. market also intensified, with the “AI Big 10” now accounting for nearly 40% of the S&P 500’s market capitalization. This concentration could intensify with the Mega-IPOs expected this year of several technology giants, including SpaceX, OpenAI and Anthropic, which could potentially be added to the S&P 500.

The AI theme is affecting a growing range of industries. Segments directly linked to digital infrastructure, including semiconductors, data centres and certain Asian supply chains, were among the quarter’s main winners once again. By contrast, traditional software companies saw their valuations decline, illustrating that the entire technology sector is not moving at the same pace and suggesting that AI can also have negative repercussions for certain business models.

In Canada, equity markets also posted strong returns, gaining nearly 7% during the second quarter. This performance nevertheless contrasts with an economy in technical recession, marked by a second consecutive quarter of declining real GDP, while U.S. tariffs—imposed by the country’s main trading partner—continue to present a challenge for many businesses.

Canadian bonds also generated positive returns during the quarter and since the start of the year. Credit spreads remained relatively tight, particularly following episodes of volatility related to geopolitical tensions, reflecting sustained demand for corporate bonds.

In the current environment, where attention is focused on both risk and surplus management, many plan sponsors and administrators are ensuring that their chosen strategies not only address current circumstances but also align with a coherent long-term path.

In this regard, pension plans can take inspiration from plans under Quebec jurisdiction, where the requirement for a funding policy is now entering its tenth year. Generally implemented at a time when plans were in deficit, this policy is now providing an opportunity to test the objectives and control mechanisms defined then in today’s surplus environment.

Although a funding policy should be reviewed periodically, its formal nature and the fact that it is established through collaboration between the sponsor and the bargaining parties help support continuity in the directions adopted as well as the preservation of intergenerational equity.

Does your plan have a funding policy? Has it been reviewed in recent years? Contact your Normandin Beaudry consultant or email us if you would like personalized support to ensure consistency between your funding objectives and your plan’s strategic directions.

The Normandin Beaudry Pension Plan Financial Position Index is calculated by projecting the pension plan financial data of its clients in the Quebec municipal and university sector. A separate index is published for the plans of Canadian clients outside of this sector. Assets are projected based on the performance of market indices. Liabilities projected on a going concern basis use an estimated discount rate based on each plan’s asset allocation and the sensitivity of asset classes to changes in interest rates on Government of Canada bonds. The rates for transfer values used on a solvency basis are those prescribed by the Canadian Institute of Actuaries and are therefore based on the previous month’s market interest rates.